சிறந்த கடன் மியூச்சுவல் ஃபண்டுகள் 2022

சிறந்த கடன் நிதிகள் முதலீட்டின் காலத்திற்கு ஏற்ப மாறுபடும்முதலீட்டாளர். முதலீட்டாளர்கள் சிறந்ததைத் தேர்ந்தெடுக்கும்போது முதலீட்டின் கால அளவைத் தெளிவாகக் கொண்டிருக்க வேண்டும்கடன் நிதி அவர்களின் முதலீடு மற்றும் வட்டி விகித சூழ்நிலையில் காரணி.

மிகக் குறைந்த ஹோல்டிங் காலம் கொண்ட முதலீட்டாளர்களுக்கு, இரண்டு நாட்கள் முதல் ஒரு மாதம் வரை சொல்லுங்கள்.திரவ நிதிகள் மற்றும் தீவிர-குறுகிய கால நிதி தொடர்புடையதாக இருக்கலாம். கால அளவு ஒன்று முதல் இரண்டு ஆண்டுகள் வரை இருக்கும் போது குறுகிய கால நிதிகள் விரும்பிய வாகனமாக இருக்கலாம். நீண்ட தவணைகளுக்கு, 3 ஆண்டுகளுக்கும் மேலாக, நீண்ட கால கடன் நிதிகள் முதலீட்டாளர்களால் மிகவும் விருப்பமான கருவிகளாகும், குறிப்பாக வட்டி விகிதங்கள் குறையும் போது. எல்லாவற்றிற்கும் மேலாக, கடன் நிதிகள் குறைவான அபாயகரமானவை என்பதை நிரூபித்துள்ளனபங்குகள் இருப்பினும், குறுகிய கால முதலீடுகளைத் தேடும் போது, நீண்ட கால வருமான நிதிகளின் ஏற்ற இறக்கம், பங்குகளுடன் பொருந்தலாம்.

கடன் நிதிகள் அரசாங்க பத்திரங்கள், கருவூல பில்கள், கார்ப்பரேட் போன்ற நிலையான வருமான கருவிகளில் முதலீடு செய்கின்றனபத்திரங்கள், முதலியன, அவை காலப்போக்கில் நிலையான மற்றும் வழக்கமான வருமானத்தை உருவாக்கும் திறனைக் கொண்டுள்ளன. எவ்வாறாயினும், முதலீடு செய்ய சிறந்த கடன் நிதிகளைத் தேர்ந்தெடுப்பதற்கு முன் ஒருவர் புரிந்து கொள்ள வேண்டிய பல தரமான மற்றும் அளவு காரணிகள் உள்ளன, அதாவது - AUM, சராசரி முதிர்வு, வரிவிதிப்பு, போர்ட்ஃபோலியோவின் கடன் தரம் போன்றவை. கீழே நாங்கள் சிறந்த 5 சிறந்த கடன் நிதிகளை பட்டியலிட்டுள்ளோம். கடன் நிதிகளின் பல்வேறு வகைகளில் முதலீடு செய்ய -சிறந்த திரவ நிதிகள், சிறந்த அல்ட்ரா குறுகிய கால நிதிகள்,சிறந்த குறுகிய கால நிதி, சிறந்த நீண்ட கால நிதி மற்றும் சிறந்ததுகில்ட் நிதிகள் 2022 - 2023 இல் முதலீடு செய்ய.

கடன் மியூச்சுவல் ஃபண்டுகளில் ஏன் முதலீடு செய்ய வேண்டும்?

அ. கடன் நிதிகள் வழக்கமான வருமானத்தை ஈட்டுவதற்கான சிறந்த முதலீடாகக் கருதப்படுகிறது. எடுத்துக்காட்டாக, டிவிடெண்ட் பேஅவுட்டைத் தேர்ந்தெடுப்பது வழக்கமான வருமானத்திற்கான ஒரு விருப்பமாக இருக்கலாம்.

பி. கடன் நிதிகளில், முதலீட்டாளர்கள் எந்த நேரத்திலும் முதலீட்டிலிருந்து தேவையான பணத்தை எடுக்கலாம் மற்றும் மீதமுள்ள பணத்தை முதலீடு செய்ய அனுமதிக்கலாம்.

c. கடன் நிதிகள் பெரும்பாலும் அரசாங்கப் பத்திரங்கள், கார்ப்பரேட் கடன் மற்றும் கருவூலப் பில்கள் போன்ற பிற பத்திரங்களில் முதலீடு செய்வதால், அவை பங்குச் சந்தை ஏற்ற இறக்கத்தால் பாதிக்கப்படுவதில்லை.

ஈ. ஒரு முதலீட்டாளர் குறுகிய காலத்தை அடைய திட்டமிட்டால்நிதி இலக்குகள் அல்லது குறுகிய காலத்திற்கு முதலீடு செய்தால் கடன் நிதிகள் ஒரு நல்ல தேர்வாக இருக்கும். திரவ நிதிகள், அல்ட்ரா குறுகிய கால நிதிகள் மற்றும் குறுகிய கால வருமான நிதிகள் ஆகியவை விரும்பிய விருப்பங்களாக இருக்கலாம்.

இ. கடன் நிதிகளில், முதலீட்டாளர்கள் ஒரு முறையான திரும்பப் பெறுதல் திட்டத்தைத் தொடங்குவதன் மூலம் ஒவ்வொரு மாதமும் நிலையான வருமானத்தை உருவாக்க முடியும் (SWPஎஸ்ஐபி /தயவு செய்து) ஒரு குறிப்பிட்ட தொகையை மாதாந்திர அடிப்படையில் திரும்பப் பெறுதல். மேலும், தேவைப்படும் போது SWP இன் அளவை மாற்றலாம்.

கடன் மியூச்சுவல் ஃபண்டுகளில் உள்ள அபாயங்கள்

போதுமுதலீடு கடன் நிதிகளில், முதலீட்டாளர்கள் அவற்றுடன் தொடர்புடைய இரண்டு முக்கிய அபாயங்களைப் பற்றி எச்சரிக்கையாக இருக்க வேண்டும் - கடன் ஆபத்து மற்றும் வட்டி ஆபத்து.

அ. கடன் ஆபத்து

கடன் கருவிகளை வழங்கிய நிறுவனம் வழக்கமான பணம் செலுத்தாதபோது கடன் ஆபத்து எழுகிறது. இதுபோன்ற சந்தர்ப்பங்களில், போர்ட்ஃபோலியோவில் நிதி எவ்வளவு பகுதியைக் கொண்டுள்ளது என்பதைப் பொறுத்து, இது நிதியில் பெரும் தாக்கத்தை ஏற்படுத்துகிறது. எனவே, அதிக கடன் மதிப்பீட்டைக் கொண்ட கடன் கருவிகளில் இருக்க பரிந்துரைக்கப்படுகிறது. ஒருAAA மதிப்பீடு சிறிய அல்லது மிகக் குறைவான கட்டணத்துடன் மிக உயர்ந்த தரமாகக் கருதப்படுகிறதுஇயல்புநிலை ஆபத்து.

பி. வட்டி அபாயங்கள்

வட்டி விகித ஆபத்து என்பது நடைமுறையில் உள்ள வட்டி விகிதத்தில் ஏற்படும் மாற்றத்தின் காரணமாக பத்திர விலையில் ஏற்படும் மாற்றத்தைக் குறிக்கிறது. பொருளாதாரத்தில் வட்டி விகிதம் உயரும்போது பத்திரங்களின் விலைகள் குறையும் மற்றும் நேர்மாறாகவும். ஃபண்டுகளின் போர்ட்ஃபோலியோவின் முதிர்வு எவ்வளவு அதிகமாக இருக்கிறதோ, அந்த அளவுக்கு அது வட்டி விகித அபாயத்திற்கு அதிக வாய்ப்புள்ளது. எனவே வட்டி விகிதம் அதிகரித்து வரும் சூழ்நிலையில், குறைந்த முதிர்வுக் கடன் நிதிகளுக்குச் செல்வது நல்லது. மற்றும் வீழ்ச்சி வட்டி விகித சூழ்நிலையில் தலைகீழ்.

கடன் மியூச்சுவல் ஃபண்ட் வரிவிதிப்பு

கடன் நிதிகள் மீதான வரி தாக்கம் பின்வரும் முறையில் கணக்கிடப்படுகிறது-

அ. குறுகிய கால மூலதன ஆதாயங்கள்

கடன் முதலீட்டின் வைத்திருக்கும் காலம் 36 மாதங்களுக்கும் குறைவாக இருந்தால், அது குறுகிய கால முதலீடாக வகைப்படுத்தப்படும், மேலும் இவை தனிநபரின் வரி அடுக்கின்படி வரி விதிக்கப்படும்.

பி. நீண்ட கால மூலதன ஆதாயங்கள்

கடன் முதலீட்டின் வைத்திருக்கும் காலம் 36 மாதங்களுக்கும் மேலாக இருந்தால், அது நீண்ட கால முதலீடாக வகைப்படுத்தப்பட்டு, குறியீட்டு நன்மையுடன் 20% வரி விதிக்கப்படும்.

| மூலதனம் ஆதாயங்கள் | முதலீட்டை வைத்திருக்கும் லாபம் | வரிவிதிப்பு |

|---|---|---|

| குறுகிய காலம்முதலீட்டு வரவுகள் | 36 மாதங்களுக்கும் குறைவானது | தனிநபரின் வரி அடுக்கு படி |

| நீண்ட கால மூலதன ஆதாயங்கள் | 36 மாதங்களுக்கு மேல் | குறியீட்டு நன்மைகளுடன் 20% |

Talk to our investment specialist

FY 22 - 23 முதலீடுகளுக்கான இந்தியாவில் சிறந்த கடன் மியூச்சுவல் ஃபண்டுகள்

முதல் 5 திரவ மியூச்சுவல் ஃபண்டுகள்

மேல்திரவம் AUM/Net Assets > 10 உடன் நிதிகள்,000 கோடி.Fund NAV Net Assets (Cr) Min Investment 1 MO (%) 3 MO (%) 6 MO (%) 1 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity Axis Liquid Fund Growth ₹3,113.75

↑ 0.64 ₹44,866 500 0.5 1.7 3.4 6.4 6.6 6.64% 1M 5D 1M 5D Aditya Birla Sun Life Liquid Fund Growth ₹450.401

↑ 0.09 ₹63,687 5,000 0.5 1.7 3.3 6.4 6.5 6.49% 2M 5D 2M 5D Invesco India Liquid Fund Growth ₹3,841.63

↑ 0.82 ₹16,797 5,000 0.5 1.7 3.3 6.4 6.5 6.56% 30D 1M 1D Nippon India Liquid Fund Growth ₹6,819.64

↑ 1.40 ₹35,870 100 0.5 1.7 3.3 6.3 6.5 6.98% 1M 14D 1M 17D Tata Liquid Fund Growth ₹4,400.79

↑ 0.96 ₹22,044 5,000 0.5 1.7 3.3 6.3 6.5 6.59% 1M 6D 1M 6D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 5 Funds showcased

Commentary Axis Liquid Fund Aditya Birla Sun Life Liquid Fund Invesco India Liquid Fund Nippon India Liquid Fund Tata Liquid Fund Point 1 Upper mid AUM (₹44,866 Cr). Highest AUM (₹63,687 Cr). Bottom quartile AUM (₹16,797 Cr). Lower mid AUM (₹35,870 Cr). Bottom quartile AUM (₹22,044 Cr). Point 2 Established history (16+ yrs). Oldest track record among peers (22 yrs). Established history (19+ yrs). Established history (22+ yrs). Established history (21+ yrs). Point 3 Top rated. Rating: 4★ (upper mid). Rating: 4★ (lower mid). Rating: 4★ (bottom quartile). Rating: 4★ (bottom quartile). Point 4 Risk profile: Low. Risk profile: Low. Risk profile: Low. Risk profile: Low. Risk profile: Low. Point 5 1Y return: 6.42% (top quartile). 1Y return: 6.37% (upper mid). 1Y return: 6.36% (lower mid). 1Y return: 6.34% (bottom quartile). 1Y return: 6.33% (bottom quartile). Point 6 1M return: 0.54% (top quartile). 1M return: 0.53% (upper mid). 1M return: 0.53% (lower mid). 1M return: 0.53% (bottom quartile). 1M return: 0.53% (bottom quartile). Point 7 Sharpe: 2.39 (top quartile). Sharpe: 2.22 (bottom quartile). Sharpe: 2.27 (lower mid). Sharpe: 2.12 (bottom quartile). Sharpe: 2.37 (upper mid). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 6.64% (upper mid). Yield to maturity (debt): 6.49% (bottom quartile). Yield to maturity (debt): 6.56% (bottom quartile). Yield to maturity (debt): 6.98% (top quartile). Yield to maturity (debt): 6.59% (lower mid). Point 10 Modified duration: 0.10 yrs (upper mid). Modified duration: 0.18 yrs (bottom quartile). Modified duration: 0.08 yrs (top quartile). Modified duration: 0.12 yrs (bottom quartile). Modified duration: 0.10 yrs (lower mid). Axis Liquid Fund

Aditya Birla Sun Life Liquid Fund

Invesco India Liquid Fund

Nippon India Liquid Fund

Tata Liquid Fund

முதல் 5 அல்ட்ரா ஷார்ட் டெர்ம் பாண்ட் மியூச்சுவல் ஃபண்டுகள்

மேல்அல்ட்ரா ஷார்ட் பாண்ட் AUM/நிகர சொத்துக்கள் > 1,000 கோடி கொண்ட நிதிகள்.Fund NAV Net Assets (Cr) Min Investment 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity Aditya Birla Sun Life Savings Fund Growth ₹588.216

↑ 0.37 ₹17,816 1,000 1.8 3.4 6.4 7.3 7.4 7.45% 5M 26D 6M 18D UTI Ultra Short Term Fund Growth ₹4,524

↑ 2.93 ₹3,146 5,000 1.8 3.2 6 6.7 6.6 7.61% 4M 1D 5M 17D ICICI Prudential Ultra Short Term Fund Growth ₹29.6777

↑ 0.02 ₹14,352 5,000 1.8 3.3 6.3 7 7.1 7.79% 5M 8D 6M 11D SBI Magnum Ultra Short Duration Fund Growth ₹6,394.59

↑ 4.13 ₹11,408 5,000 1.8 3.3 6.2 7 7 7.77% 5M 5D 8M 16D Invesco India Ultra Short Term Fund Growth ₹2,883.94

↑ 1.80 ₹1,002 5,000 1.8 3.3 6.1 6.9 6.8 7.53% 5M 3D 5M 6D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 5 Funds showcased

Commentary Aditya Birla Sun Life Savings Fund UTI Ultra Short Term Fund ICICI Prudential Ultra Short Term Fund SBI Magnum Ultra Short Duration Fund Invesco India Ultra Short Term Fund Point 1 Highest AUM (₹17,816 Cr). Bottom quartile AUM (₹3,146 Cr). Upper mid AUM (₹14,352 Cr). Lower mid AUM (₹11,408 Cr). Bottom quartile AUM (₹1,002 Cr). Point 2 Established history (23+ yrs). Established history (22+ yrs). Established history (15+ yrs). Oldest track record among peers (27 yrs). Established history (15+ yrs). Point 3 Top rated. Rating: 4★ (upper mid). Rating: 3★ (lower mid). Rating: 3★ (bottom quartile). Rating: 3★ (bottom quartile). Point 4 Risk profile: Moderately Low. Risk profile: Moderately Low. Risk profile: Moderate. Risk profile: Low. Risk profile: Moderate. Point 5 1Y return: 6.36% (top quartile). 1Y return: 5.96% (bottom quartile). 1Y return: 6.30% (upper mid). 1Y return: 6.22% (lower mid). 1Y return: 6.13% (bottom quartile). Point 6 1M return: 0.61% (top quartile). 1M return: 0.55% (bottom quartile). 1M return: 0.58% (upper mid). 1M return: 0.56% (lower mid). 1M return: 0.55% (bottom quartile). Point 7 Sharpe: 0.91 (upper mid). Sharpe: 0.43 (bottom quartile). Sharpe: 0.92 (top quartile). Sharpe: 0.84 (lower mid). Sharpe: 0.68 (bottom quartile). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 7.45% (bottom quartile). Yield to maturity (debt): 7.61% (lower mid). Yield to maturity (debt): 7.79% (top quartile). Yield to maturity (debt): 7.77% (upper mid). Yield to maturity (debt): 7.53% (bottom quartile). Point 10 Modified duration: 0.49 yrs (bottom quartile). Modified duration: 0.34 yrs (top quartile). Modified duration: 0.44 yrs (bottom quartile). Modified duration: 0.43 yrs (lower mid). Modified duration: 0.42 yrs (upper mid). Aditya Birla Sun Life Savings Fund

UTI Ultra Short Term Fund

ICICI Prudential Ultra Short Term Fund

SBI Magnum Ultra Short Duration Fund

Invesco India Ultra Short Term Fund

சிறந்த மற்றும் சிறந்த மிதக்கும் விகித மியூச்சுவல் ஃபண்டுகள்

Fund NAV Net Assets (Cr) Min Investment 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity Aditya Birla Sun Life Floating Rate Fund - Long Term Growth ₹372.654

↑ 0.26 ₹13,519 1,000 1.9 3.3 6.1 7.3 7.7 7.21% 10M 28D 1Y 8M 26D ICICI Prudential Floating Interest Fund Growth ₹456.024

↑ 0.38 ₹8,011 5,000 2.1 3.5 6.5 7.5 7.7 7.87% 1Y 10M 13D 2Y 10M 24D Nippon India Floating Rate Fund Growth ₹48.2965

↑ 0.04 ₹7,626 5,000 2.2 3.3 5.7 7.4 7.9 7.9% 2Y 2M 1D 2Y 8M 1D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 3 Funds showcased

Commentary Aditya Birla Sun Life Floating Rate Fund - Long Term ICICI Prudential Floating Interest Fund Nippon India Floating Rate Fund Point 1 Highest AUM (₹13,519 Cr). Lower mid AUM (₹8,011 Cr). Bottom quartile AUM (₹7,626 Cr). Point 2 Established history (17+ yrs). Established history (20+ yrs). Oldest track record among peers (21 yrs). Point 3 Top rated. Rating: 3★ (lower mid). Rating: 3★ (bottom quartile). Point 4 Risk profile: Moderately Low. Risk profile: Moderate. Risk profile: Moderately Low. Point 5 1Y return: 6.11% (lower mid). 1Y return: 6.48% (upper mid). 1Y return: 5.71% (bottom quartile). Point 6 1M return: 0.57% (upper mid). 1M return: 0.56% (bottom quartile). 1M return: 0.56% (lower mid). Point 7 Sharpe: 0.48 (lower mid). Sharpe: 0.63 (upper mid). Sharpe: 0.11 (bottom quartile). Point 8 Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 7.21% (bottom quartile). Yield to maturity (debt): 7.87% (lower mid). Yield to maturity (debt): 7.90% (upper mid). Point 10 Modified duration: 0.91 yrs (upper mid). Modified duration: 1.87 yrs (lower mid). Modified duration: 2.17 yrs (bottom quartile). Aditya Birla Sun Life Floating Rate Fund - Long Term

ICICI Prudential Floating Interest Fund

Nippon India Floating Rate Fund

முதல் 5 சிறந்த பணச் சந்தை மியூச்சுவல் ஃபண்டுகள்

Fund NAV Net Assets (Cr) Min Investment 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity Aditya Birla Sun Life Money Manager Fund Growth ₹397.18

↑ 0.29 ₹27,383 1,000 1.9 3.4 6.3 7.3 7.4 6.95% 6M 25D 6M 29D UTI Money Market Fund Growth ₹3,311.52

↑ 2.37 ₹17,557 10,000 1.9 3.4 6.4 7.3 7.5 7.58% 6M 20D 6M 20D Kotak Money Market Scheme Growth ₹4,819.75

↑ 3.30 ₹28,762 5,000 1.9 3.4 6.3 7.3 7.4 7.71% 7M 6D 7M 6D ICICI Prudential Money Market Fund Growth ₹407.264

↑ 0.28 ₹31,085 500 1.8 3.3 6.3 7.3 7.4 7.7% 6M 29D 7M 16D Tata Money Market Fund Growth ₹5,068.45

↑ 3.52 ₹32,150 5,000 1.8 3.4 6.3 7.3 7.4 7.79% 7M 1D 7M 1D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 5 Funds showcased

Commentary Aditya Birla Sun Life Money Manager Fund UTI Money Market Fund Kotak Money Market Scheme ICICI Prudential Money Market Fund Tata Money Market Fund Point 1 Bottom quartile AUM (₹27,383 Cr). Bottom quartile AUM (₹17,557 Cr). Lower mid AUM (₹28,762 Cr). Upper mid AUM (₹31,085 Cr). Highest AUM (₹32,150 Cr). Point 2 Established history (20+ yrs). Established history (17+ yrs). Oldest track record among peers (23 yrs). Established history (20+ yrs). Established history (23+ yrs). Point 3 Top rated. Rating: 4★ (upper mid). Rating: 4★ (lower mid). Rating: 4★ (bottom quartile). Rating: 3★ (bottom quartile). Point 4 Risk profile: Low. Risk profile: Low. Risk profile: Low. Risk profile: Low. Risk profile: Low. Point 5 1Y return: 6.35% (upper mid). 1Y return: 6.39% (top quartile). 1Y return: 6.34% (bottom quartile). 1Y return: 6.32% (bottom quartile). 1Y return: 6.34% (lower mid). Point 6 1M return: 0.62% (upper mid). 1M return: 0.62% (top quartile). 1M return: 0.61% (bottom quartile). 1M return: 0.62% (lower mid). 1M return: 0.61% (bottom quartile). Point 7 Sharpe: 0.69 (bottom quartile). Sharpe: 0.81 (upper mid). Sharpe: 0.75 (lower mid). Sharpe: 0.72 (bottom quartile). Sharpe: 0.82 (top quartile). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 6.95% (bottom quartile). Yield to maturity (debt): 7.58% (bottom quartile). Yield to maturity (debt): 7.71% (upper mid). Yield to maturity (debt): 7.70% (lower mid). Yield to maturity (debt): 7.79% (top quartile). Point 10 Modified duration: 0.57 yrs (upper mid). Modified duration: 0.56 yrs (top quartile). Modified duration: 0.60 yrs (bottom quartile). Modified duration: 0.58 yrs (lower mid). Modified duration: 0.59 yrs (bottom quartile). Aditya Birla Sun Life Money Manager Fund

UTI Money Market Fund

Kotak Money Market Scheme

ICICI Prudential Money Market Fund

Tata Money Market Fund

முதல் 5 குறுகிய கால பாண்ட் மியூச்சுவல் ஃபண்டுகள்

Fund NAV Net Assets (Cr) 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity PGIM India Short Maturity Fund Growth ₹39.3202

↓ 0.00 ₹28 1.2 3.1 6.1 4.2 7.18% 1Y 7M 28D 1Y 11M 1D ICICI Prudential Short Term Fund Growth ₹64.4502

↑ 0.06 ₹19,175 2.3 3.5 6.1 7.4 8 8.14% 2Y 8M 19D 4Y 5M 23D Aditya Birla Sun Life Short Term Opportunities Fund Growth ₹50.7297

↑ 0.04 ₹5,793 2.3 3.2 5.6 7.2 7.7 7.76% 2Y 8M 16D 3Y 6M 18D Nippon India Short Term Fund Growth ₹56.3324

↑ 0.04 ₹7,040 2.3 3.2 5.5 7.3 7.9 8.03% 2Y 3M 18D 2Y 8M 23D UTI Short Term Income Fund Growth ₹33.7375

↑ 0.02 ₹2,128 2.2 3.2 5.4 7.1 7.3 7.92% 1Y 9M 7D 2Y 8M 19D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 29 Sep 23 Research Highlights & Commentary of 5 Funds showcased

Commentary PGIM India Short Maturity Fund ICICI Prudential Short Term Fund Aditya Birla Sun Life Short Term Opportunities Fund Nippon India Short Term Fund UTI Short Term Income Fund Point 1 Bottom quartile AUM (₹28 Cr). Highest AUM (₹19,175 Cr). Lower mid AUM (₹5,793 Cr). Upper mid AUM (₹7,040 Cr). Bottom quartile AUM (₹2,128 Cr). Point 2 Established history (23+ yrs). Oldest track record among peers (24 yrs). Established history (23+ yrs). Established history (23+ yrs). Established history (18+ yrs). Point 3 Top rated. Rating: 4★ (upper mid). Rating: 4★ (lower mid). Rating: 4★ (bottom quartile). Rating: 4★ (bottom quartile). Point 4 Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderately Low. Risk profile: Moderate. Point 5 1Y return: 6.08% (top quartile). 1Y return: 6.07% (upper mid). 1Y return: 5.59% (lower mid). 1Y return: 5.53% (bottom quartile). 1Y return: 5.35% (bottom quartile). Point 6 1M return: 0.43% (bottom quartile). 1M return: 0.49% (bottom quartile). 1M return: 0.52% (lower mid). 1M return: 0.56% (upper mid). 1M return: 0.57% (top quartile). Point 7 Sharpe: -0.98 (bottom quartile). Sharpe: 0.29 (top quartile). Sharpe: 0.05 (upper mid). Sharpe: 0.00 (lower mid). Sharpe: -0.17 (bottom quartile). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 7.18% (bottom quartile). Yield to maturity (debt): 8.14% (top quartile). Yield to maturity (debt): 7.76% (bottom quartile). Yield to maturity (debt): 8.03% (upper mid). Yield to maturity (debt): 7.92% (lower mid). Point 10 Modified duration: 1.66 yrs (top quartile). Modified duration: 2.72 yrs (bottom quartile). Modified duration: 2.71 yrs (bottom quartile). Modified duration: 2.30 yrs (lower mid). Modified duration: 1.77 yrs (upper mid). PGIM India Short Maturity Fund

ICICI Prudential Short Term Fund

Aditya Birla Sun Life Short Term Opportunities Fund

Nippon India Short Term Fund

UTI Short Term Income Fund

முதல் 5 நடுத்தர முதல் நீண்ட கால பாண்ட் மியூச்சுவல் ஃபண்டுகள்

மேல்நடுத்தர முதல் நீண்ட கால பத்திரம் AUM/நிகர சொத்துக்கள் > 500 கோடி கொண்ட நிதி.Fund NAV Net Assets (Cr) 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity SBI Magnum Income Fund Growth ₹74.0962

↑ 0.07 ₹2,055 2.5 3.4 4.6 6.5 5.9 7.92% 4Y 1M 17D 8Y 3M ICICI Prudential Bond Fund Growth ₹42.477

↑ 0.05 ₹2,002 2.9 4 5 7.2 6.7 7.85% 6Y 5M 19D 15Y 2M 16D Aditya Birla Sun Life Income Fund Growth ₹130.687

↑ 0.19 ₹1,787 2.8 3.5 3.9 6.2 5.1 7.47% 6Y 8M 5D 15Y 18D Kotak Bond Fund Growth ₹80.4651

↑ 0.08 ₹1,807 3.2 3.7 4.6 6.5 5.4 7.59% 4Y 7M 20D 8Y 2M 5D HDFC Income Fund Growth ₹60.9309

↑ 0.09 ₹833 3.1 3.8 4.6 6.7 5.5 7.34% 6Y 5M 8D 13Y 1M 28D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 5 Funds showcased

Commentary SBI Magnum Income Fund ICICI Prudential Bond Fund Aditya Birla Sun Life Income Fund Kotak Bond Fund HDFC Income Fund Point 1 Highest AUM (₹2,055 Cr). Upper mid AUM (₹2,002 Cr). Bottom quartile AUM (₹1,787 Cr). Lower mid AUM (₹1,807 Cr). Bottom quartile AUM (₹833 Cr). Point 2 Established history (27+ yrs). Established history (17+ yrs). Oldest track record among peers (30 yrs). Established history (26+ yrs). Established history (25+ yrs). Point 3 Top rated. Rating: 3★ (upper mid). Rating: 3★ (lower mid). Rating: 2★ (bottom quartile). Rating: 2★ (bottom quartile). Point 4 Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderate. Point 5 1Y return: 4.56% (bottom quartile). 1Y return: 5.03% (top quartile). 1Y return: 3.87% (bottom quartile). 1Y return: 4.59% (upper mid). 1Y return: 4.57% (lower mid). Point 6 1M return: 0.29% (lower mid). 1M return: 0.31% (upper mid). 1M return: 0.27% (bottom quartile). 1M return: 0.37% (top quartile). 1M return: 0.28% (bottom quartile). Point 7 Sharpe: -0.40 (bottom quartile). Sharpe: -0.21 (top quartile). Sharpe: -0.49 (bottom quartile). Sharpe: -0.39 (lower mid). Sharpe: -0.37 (upper mid). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 7.92% (top quartile). Yield to maturity (debt): 7.85% (upper mid). Yield to maturity (debt): 7.47% (bottom quartile). Yield to maturity (debt): 7.59% (lower mid). Yield to maturity (debt): 7.34% (bottom quartile). Point 10 Modified duration: 4.13 yrs (top quartile). Modified duration: 6.47 yrs (bottom quartile). Modified duration: 6.68 yrs (bottom quartile). Modified duration: 4.64 yrs (upper mid). Modified duration: 6.44 yrs (lower mid). SBI Magnum Income Fund

ICICI Prudential Bond Fund

Aditya Birla Sun Life Income Fund

Kotak Bond Fund

HDFC Income Fund

முதல் 5 வங்கி மற்றும் PSU கடன் பரஸ்பர நிதிகள்

Fund NAV Net Assets (Cr) 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity UTI Banking & PSU Debt Fund Growth ₹23.4183

↑ 0.02 ₹1,101 1.8 3.2 5.7 7.2 7.8 7.69% 9M 14D 10M 2D HDFC Banking and PSU Debt Fund Growth ₹24.4474

↑ 0.02 ₹5,255 2.4 3.2 5.2 7 7.5 7.78% 3Y 7D 4Y 1M 2D ICICI Prudential Banking and PSU Debt Fund Growth ₹34.9247

↑ 0.03 ₹8,823 2.3 3.4 5.8 7.2 7.6 7.9% 3Y 2M 16D 5Y 9M 29D Kotak Banking and PSU Debt fund Growth ₹69.7188

↑ 0.05 ₹5,019 2.3 3.2 5.7 7.2 7.7 7.77% 2Y 9M 22D 3Y 6M 18D Aditya Birla Sun Life Banking & PSU Debt Fund Growth ₹388.602

↑ 0.35 ₹8,963 2.1 3.1 5 7 7.3 7.22% 3Y 18D 4Y 4M 28D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 5 Funds showcased

Commentary UTI Banking & PSU Debt Fund HDFC Banking and PSU Debt Fund ICICI Prudential Banking and PSU Debt Fund Kotak Banking and PSU Debt fund Aditya Birla Sun Life Banking & PSU Debt Fund Point 1 Bottom quartile AUM (₹1,101 Cr). Lower mid AUM (₹5,255 Cr). Upper mid AUM (₹8,823 Cr). Bottom quartile AUM (₹5,019 Cr). Highest AUM (₹8,963 Cr). Point 2 Established history (12+ yrs). Established history (12+ yrs). Established history (16+ yrs). Oldest track record among peers (27 yrs). Established history (18+ yrs). Point 3 Top rated. Rating: 5★ (upper mid). Rating: 4★ (lower mid). Rating: 4★ (bottom quartile). Rating: 4★ (bottom quartile). Point 4 Risk profile: Moderate. Risk profile: Moderately Low. Risk profile: Moderate. Risk profile: Moderately Low. Risk profile: Moderate. Point 5 1Y return: 5.70% (upper mid). 1Y return: 5.25% (bottom quartile). 1Y return: 5.79% (top quartile). 1Y return: 5.65% (lower mid). 1Y return: 4.99% (bottom quartile). Point 6 1M return: 0.60% (top quartile). 1M return: 0.51% (upper mid). 1M return: 0.49% (bottom quartile). 1M return: 0.50% (lower mid). 1M return: 0.44% (bottom quartile). Point 7 Sharpe: 0.07 (upper mid). Sharpe: -0.11 (bottom quartile). Sharpe: 0.12 (top quartile). Sharpe: 0.04 (lower mid). Sharpe: -0.23 (bottom quartile). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 7.69% (bottom quartile). Yield to maturity (debt): 7.78% (upper mid). Yield to maturity (debt): 7.90% (top quartile). Yield to maturity (debt): 7.77% (lower mid). Yield to maturity (debt): 7.22% (bottom quartile). Point 10 Modified duration: 0.79 yrs (top quartile). Modified duration: 3.02 yrs (lower mid). Modified duration: 3.21 yrs (bottom quartile). Modified duration: 2.81 yrs (upper mid). Modified duration: 3.05 yrs (bottom quartile). UTI Banking & PSU Debt Fund

HDFC Banking and PSU Debt Fund

ICICI Prudential Banking and PSU Debt Fund

Kotak Banking and PSU Debt fund

Aditya Birla Sun Life Banking & PSU Debt Fund

முதல் 5 கிரெடிட் ரிஸ்க் மியூச்சுவல் ஃபண்டுகள்

மேல்கடன் ஆபத்து AUM/நிகர சொத்துக்கள் > 500 கோடி கொண்ட நிதி.Fund NAV Net Assets (Cr) 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity SBI Credit Risk Fund Growth ₹49.6047

↑ 0.05 ₹2,175 3.1 4.7 7.7 8 7.9 8.7% 2Y 22D 2Y 8M 23D HDFC Credit Risk Debt Fund Growth ₹26.035

↑ 0.03 ₹7,693 2.7 4.2 7.3 7.8 8 8.8% 2Y 2M 23D 3Y 5M 23D Kotak Credit Risk Fund Growth ₹31.9222

↑ 0.04 ₹768 2.7 3.4 7.4 7.8 9.1 8.95% 1Y 11M 5D 2Y 11M 5D Nippon India Credit Risk Fund Growth ₹38.018

↑ 0.03 ₹1,486 2.4 4.1 7.3 8.2 8.9 9.12% 2Y 11D 2Y 5M 5D ICICI Prudential Regular Savings Fund Growth ₹34.7927

↑ 0.03 ₹6,212 2.9 3.9 8.4 8.5 9.5 8.93% 2Y 14D 3Y 1M 10D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 5 Funds showcased

Commentary SBI Credit Risk Fund HDFC Credit Risk Debt Fund Kotak Credit Risk Fund Nippon India Credit Risk Fund ICICI Prudential Regular Savings Fund Point 1 Lower mid AUM (₹2,175 Cr). Highest AUM (₹7,693 Cr). Bottom quartile AUM (₹768 Cr). Bottom quartile AUM (₹1,486 Cr). Upper mid AUM (₹6,212 Cr). Point 2 Oldest track record among peers (22 yrs). Established history (12+ yrs). Established history (16+ yrs). Established history (21+ yrs). Established history (15+ yrs). Point 3 Top rated. Rating: 4★ (upper mid). Rating: 3★ (lower mid). Rating: 2★ (bottom quartile). Rating: 1★ (bottom quartile). Point 4 Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderately Low. Risk profile: Moderate. Risk profile: Moderate. Point 5 1Y return: 7.70% (upper mid). 1Y return: 7.30% (bottom quartile). 1Y return: 7.43% (lower mid). 1Y return: 7.30% (bottom quartile). 1Y return: 8.43% (top quartile). Point 6 1M return: 0.84% (top quartile). 1M return: 0.82% (upper mid). 1M return: 0.82% (lower mid). 1M return: 0.67% (bottom quartile). 1M return: 0.80% (bottom quartile). Point 7 Sharpe: 1.03 (lower mid). Sharpe: 0.73 (bottom quartile). Sharpe: 0.66 (bottom quartile). Sharpe: 1.22 (upper mid). Sharpe: 1.40 (top quartile). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 8.70% (bottom quartile). Yield to maturity (debt): 8.80% (bottom quartile). Yield to maturity (debt): 8.95% (upper mid). Yield to maturity (debt): 9.12% (top quartile). Yield to maturity (debt): 8.93% (lower mid). Point 10 Modified duration: 2.06 yrs (bottom quartile). Modified duration: 2.23 yrs (bottom quartile). Modified duration: 1.93 yrs (top quartile). Modified duration: 2.03 yrs (upper mid). Modified duration: 2.04 yrs (lower mid). SBI Credit Risk Fund

HDFC Credit Risk Debt Fund

Kotak Credit Risk Fund

Nippon India Credit Risk Fund

ICICI Prudential Regular Savings Fund

டாப் 5 டைனமிக் பாண்ட் மியூச்சுவல் ஃபண்டுகள்

மேல்டைனமிக் பாண்ட் AUM/நிகர சொத்துக்கள் > 500 கோடி கொண்ட நிதி.Fund NAV Net Assets (Cr) 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity SBI Dynamic Bond Fund Growth ₹37.5602

↑ 0.03 ₹3,752 2 3.6 4.9 6.8 5.5 7.82% 3Y 7M 13D 5Y 4M 24D Bandhan Dynamic Bond Fund Growth ₹35.949

↑ 0.09 ₹2,007 3.6 5.3 6.8 7 3.4 7.71% 7Y 11M 23D 21Y 3M 14D Axis Dynamic Bond Fund Growth ₹31.6417

↑ 0.04 ₹1,015 2.9 4.5 6.3 7.4 7.1 7.26% 5Y 10Y 9M 14D Aditya Birla Sun Life Dynamic Bond Fund Growth ₹49.1515

↑ 0.06 ₹1,495 2.7 3.8 5.4 7.3 7 8.08% 5Y 3M 18D 11Y 11M 8D HDFC Dynamic Debt Fund Growth ₹93.8575

↑ 0.20 ₹532 3.2 4.3 4.9 6.5 4.7 7.53% 7Y 4M 24D 19Y 8M 26D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 5 Funds showcased

Commentary SBI Dynamic Bond Fund Bandhan Dynamic Bond Fund Axis Dynamic Bond Fund Aditya Birla Sun Life Dynamic Bond Fund HDFC Dynamic Debt Fund Point 1 Highest AUM (₹3,752 Cr). Upper mid AUM (₹2,007 Cr). Bottom quartile AUM (₹1,015 Cr). Lower mid AUM (₹1,495 Cr). Bottom quartile AUM (₹532 Cr). Point 2 Established history (22+ yrs). Established history (17+ yrs). Established history (15+ yrs). Established history (21+ yrs). Oldest track record among peers (29 yrs). Point 3 Top rated. Rating: 3★ (upper mid). Rating: 3★ (lower mid). Rating: 3★ (bottom quartile). Rating: 3★ (bottom quartile). Point 4 Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderate. Point 5 1Y return: 4.94% (bottom quartile). 1Y return: 6.79% (top quartile). 1Y return: 6.35% (upper mid). 1Y return: 5.44% (lower mid). 1Y return: 4.93% (bottom quartile). Point 6 1M return: 0.36% (upper mid). 1M return: -0.25% (bottom quartile). 1M return: 0.31% (lower mid). 1M return: 0.27% (bottom quartile). 1M return: 0.61% (top quartile). Point 7 Sharpe: -0.48 (bottom quartile). Sharpe: 0.28 (top quartile). Sharpe: 0.14 (upper mid). Sharpe: -0.06 (lower mid). Sharpe: -0.34 (bottom quartile). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 7.82% (upper mid). Yield to maturity (debt): 7.71% (lower mid). Yield to maturity (debt): 7.26% (bottom quartile). Yield to maturity (debt): 8.08% (top quartile). Yield to maturity (debt): 7.53% (bottom quartile). Point 10 Modified duration: 3.62 yrs (top quartile). Modified duration: 7.98 yrs (bottom quartile). Modified duration: 5.00 yrs (upper mid). Modified duration: 5.30 yrs (lower mid). Modified duration: 7.40 yrs (bottom quartile). SBI Dynamic Bond Fund

Bandhan Dynamic Bond Fund

Axis Dynamic Bond Fund

Aditya Birla Sun Life Dynamic Bond Fund

HDFC Dynamic Debt Fund

முதல் 5 கார்ப்பரேட் பாண்ட் மியூச்சுவல் ஃபண்டுகள்

மேல்கார்ப்பரேட் பாண்ட் AUM/நிகர சொத்துக்கள் > 500 கோடி கொண்ட நிதி.Fund NAV Net Assets (Cr) 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity Aditya Birla Sun Life Corporate Bond Fund Growth ₹119.892

↑ 0.12 ₹23,841 2.5 3.4 5.3 7.3 7.4 7.34% 4Y 1M 6D 6Y 7M 28D HDFC Corporate Bond Fund Growth ₹34.5292

↑ 0.03 ₹30,721 2.6 3.4 5.1 7.2 7.3 7.79% 4Y 18D 6Y 11M 12D ICICI Prudential Corporate Bond Fund Growth ₹31.9948

↑ 0.03 ₹30,030 2.5 3.7 6.2 7.5 8 7.91% 3Y 4M 10D 5Y 8M 23D Kotak Corporate Bond Fund Standard Growth ₹4,016.89

↑ 3.75 ₹14,997 2.3 3.2 5.4 7.3 7.8 7.99% 2Y 6M 29D 4Y Nippon India Prime Debt Fund Growth ₹63.8916

↑ 0.05 ₹9,433 2.4 3.3 5.3 7.4 7.8 7.9% 2Y 4M 6D 2Y 10M 13D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 5 Funds showcased

Commentary Aditya Birla Sun Life Corporate Bond Fund HDFC Corporate Bond Fund ICICI Prudential Corporate Bond Fund Kotak Corporate Bond Fund Standard Nippon India Prime Debt Fund Point 1 Lower mid AUM (₹23,841 Cr). Highest AUM (₹30,721 Cr). Upper mid AUM (₹30,030 Cr). Bottom quartile AUM (₹14,997 Cr). Bottom quartile AUM (₹9,433 Cr). Point 2 Oldest track record among peers (29 yrs). Established history (16+ yrs). Established history (17+ yrs). Established history (18+ yrs). Established history (25+ yrs). Point 3 Top rated. Rating: 5★ (upper mid). Rating: 4★ (lower mid). Rating: 4★ (bottom quartile). Rating: 4★ (bottom quartile). Point 4 Risk profile: Moderately Low. Risk profile: Moderately Low. Risk profile: Moderately Low. Risk profile: Moderately Low. Risk profile: Moderately Low. Point 5 1Y return: 5.29% (bottom quartile). 1Y return: 5.11% (bottom quartile). 1Y return: 6.22% (top quartile). 1Y return: 5.36% (upper mid). 1Y return: 5.30% (lower mid). Point 6 1M return: 0.41% (bottom quartile). 1M return: 0.44% (bottom quartile). 1M return: 0.50% (upper mid). 1M return: 0.50% (lower mid). 1M return: 0.55% (top quartile). Point 7 Sharpe: -0.10 (lower mid). Sharpe: -0.14 (bottom quartile). Sharpe: 0.31 (top quartile). Sharpe: -0.10 (upper mid). Sharpe: -0.12 (bottom quartile). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 7.34% (bottom quartile). Yield to maturity (debt): 7.79% (bottom quartile). Yield to maturity (debt): 7.91% (upper mid). Yield to maturity (debt): 7.99% (top quartile). Yield to maturity (debt): 7.90% (lower mid). Point 10 Modified duration: 4.10 yrs (bottom quartile). Modified duration: 4.05 yrs (bottom quartile). Modified duration: 3.36 yrs (lower mid). Modified duration: 2.58 yrs (upper mid). Modified duration: 2.35 yrs (top quartile). Aditya Birla Sun Life Corporate Bond Fund

HDFC Corporate Bond Fund

ICICI Prudential Corporate Bond Fund

Kotak Corporate Bond Fund Standard

Nippon India Prime Debt Fund

சிறந்த 5 கில்ட் மியூச்சுவல் ஃபண்டுகள்

மேல் (Erstwhile DHFL Pramerica Credit Opportunities Fund) The investment objective of the Scheme is to generate income and capital appreciation by investing predominantly in corporate debt. There can be no assurance that the investment objective of the Scheme will be realized. Research Highlights for PGIM India Credit Risk Fund Below is the key information for PGIM India Credit Risk Fund Returns up to 1 year are on (Erstwhile Axis Fixed Income Opportunities Fund) To generate stable returns by investing in debt & money market instruments across the yield curve & credit spectrum. However, there is no assurance or guarantee that the investment objective of the Scheme will be achieved. The Scheme does not assure or guarantee any returns Research Highlights for Axis Credit Risk Fund Below is the key information for Axis Credit Risk Fund Returns up to 1 year are on (Erstwhile DHFL Pramerica Insta Cash Plus Fund) To generate steady returns along with high liquidity by investing in a portfolio of short-term, high quality money market and debt instruments. Research Highlights for PGIM India Insta Cash Fund Below is the key information for PGIM India Insta Cash Fund Returns up to 1 year are on The primary objective of the schemes is to generate regular income through investments in debt and money market instruments. Income maybe generated through the receipt of coupon payments or the purchase and sale of securities in the underlying portfolio. The schemes will under normal market conditions, invest its net assets in fixed income securities, money market instruments, cash and cash equivalents. Research Highlights for Aditya Birla Sun Life Savings Fund Below is the key information for Aditya Birla Sun Life Savings Fund Returns up to 1 year are on (Erstwhile Aditya Birla Sun Life Floating Rate Fund - Short Term) The primary objective of the schemes is to generate regular income through investment in a portfolio comprising substantially of floating rate debt / money market instruments. The schemes may invest a portion of its net assets in fixed rate debt securities and money market instruments. Research Highlights for Aditya Birla Sun Life Money Manager Fund Below is the key information for Aditya Birla Sun Life Money Manager Fund Returns up to 1 year are on பொருந்தும் AUM/நிகர சொத்துக்கள் > 500 கோடி கொண்ட நிதி.Fund NAV Net Assets (Cr) 3 MO (%) 6 MO (%) 1 YR (%) 3 YR (%) 2025 (%) Debt Yield (YTM) Mod. Duration Eff. Maturity ICICI Prudential Gilt Fund Growth ₹108.85

↑ 0.16 ₹8,785 3.4 4.5 5.3 7.2 6.8 7.71% 9Y 4M 10D 21Y 7M 6D SBI Magnum Constant Maturity Fund Growth ₹66.9928

↑ 0.05 ₹1,666 3.3 3.5 4.8 7.2 6.7 7.23% 6Y 9M 14D 9Y 6M 11D SBI Magnum Gilt Fund Growth ₹68.5427

↑ 0.12 ₹8,455 2.3 3.2 3.9 6.4 4.5 6.89% 5Y 10M 28D 10Y 1M 20D Nippon India Gilt Securities Fund Growth ₹39.3439

↑ 0.08 ₹1,592 3.1 4.1 3.9 6.1 3.7 7.45% 8Y 7M 28D 21Y 3M 14D Aditya Birla Sun Life Government Securities Fund Growth ₹82.5399

↑ 0.22 ₹1,376 2.9 3.6 2.5 5.6 3 7.49% 11Y 7M 20D 33Y 6M 18D Note: Returns up to 1 year are on absolute basis & more than 1 year are on CAGR basis. as on 10 Aug 26 Research Highlights & Commentary of 5 Funds showcased

Commentary ICICI Prudential Gilt Fund SBI Magnum Constant Maturity Fund SBI Magnum Gilt Fund Nippon India Gilt Securities Fund Aditya Birla Sun Life Government Securities Fund Point 1 Highest AUM (₹8,785 Cr). Lower mid AUM (₹1,666 Cr). Upper mid AUM (₹8,455 Cr). Bottom quartile AUM (₹1,592 Cr). Bottom quartile AUM (₹1,376 Cr). Point 2 Oldest track record among peers (26 yrs). Established history (25+ yrs). Established history (25+ yrs). Established history (17+ yrs). Established history (26+ yrs). Point 3 Top rated. Rating: 4★ (upper mid). Rating: 4★ (lower mid). Rating: 4★ (bottom quartile). Rating: 4★ (bottom quartile). Point 4 Risk profile: Moderate. Risk profile: Moderately Low. Risk profile: Moderate. Risk profile: Moderate. Risk profile: Moderate. Point 5 1Y return: 5.35% (top quartile). 1Y return: 4.80% (upper mid). 1Y return: 3.93% (lower mid). 1Y return: 3.87% (bottom quartile). 1Y return: 2.46% (bottom quartile). Point 6 1M return: 0.20% (upper mid). 1M return: 0.22% (top quartile). 1M return: 0.06% (lower mid). 1M return: -0.02% (bottom quartile). 1M return: -0.28% (bottom quartile). Point 7 Sharpe: -0.14 (top quartile). Sharpe: -0.42 (lower mid). Sharpe: -0.51 (bottom quartile). Sharpe: -0.37 (upper mid). Sharpe: -0.42 (bottom quartile). Point 8 Information ratio: 0.00 (top quartile). Information ratio: 0.00 (upper mid). Information ratio: 0.00 (lower mid). Information ratio: 0.00 (bottom quartile). Information ratio: 0.00 (bottom quartile). Point 9 Yield to maturity (debt): 7.71% (top quartile). Yield to maturity (debt): 7.23% (bottom quartile). Yield to maturity (debt): 6.89% (bottom quartile). Yield to maturity (debt): 7.45% (lower mid). Yield to maturity (debt): 7.49% (upper mid). Point 10 Modified duration: 9.36 yrs (bottom quartile). Modified duration: 6.79 yrs (upper mid). Modified duration: 5.91 yrs (top quartile). Modified duration: 8.66 yrs (lower mid). Modified duration: 11.64 yrs (bottom quartile). ICICI Prudential Gilt Fund

SBI Magnum Constant Maturity Fund

SBI Magnum Gilt Fund

Nippon India Gilt Securities Fund

Aditya Birla Sun Life Government Securities Fund

1. PGIM India Credit Risk Fund

PGIM India Credit Risk Fund

Growth Launch Date 29 Sep 14 NAV (21 Jan 22) ₹15.5876 ↑ 0.00 (0.01 %) Net Assets (Cr) ₹39 on 31 Dec 21 Category Debt - Credit Risk AMC Pramerica Asset Managers Private Limited Rating ☆☆☆☆☆ Risk Moderate Expense Ratio 1.85 Sharpe Ratio 1.73 Information Ratio 0 Alpha Ratio 0 Min Investment 5,000 Min SIP Investment 1,000 Exit Load 0-1 Years (1%),1 Years and above(NIL) Yield to Maturity 5.01% Effective Maturity 7 Months 2 Days Modified Duration 6 Months 14 Days Growth of 10,000 investment over the years.

Date Value Returns for PGIM India Credit Risk Fund

absolute basis & more than 1 year are on CAGR (Compound Annual Growth Rate) basis. as on 21 Jan 22 Duration Returns 1 Month 0.3% 3 Month 0.6% 6 Month 4.4% 1 Year 8.4% 3 Year 3% 5 Year 4.2% 10 Year 15 Year Since launch 6.3% Historical performance (Yearly) on absolute basis

Year Returns 2025 2024 2023 2022 2021 2020 2019 2018 2017 2016 Fund Manager information for PGIM India Credit Risk Fund

Name Since Tenure Data below for PGIM India Credit Risk Fund as on 31 Dec 21

Asset Allocation

Asset Class Value Debt Sector Allocation

Sector Value Credit Quality

Rating Value Top Securities Holdings / Portfolio

Name Holding Value Quantity 2. Axis Credit Risk Fund

Axis Credit Risk Fund

Growth Launch Date 15 Jul 14 NAV (10 Aug 26) ₹23.373 ↑ 0.02 (0.09 %) Net Assets (Cr) ₹362 on 30 Jun 26 Category Debt - Credit Risk AMC Axis Asset Management Company Limited Rating ☆☆☆☆☆ Risk Moderate Expense Ratio 1.57 Sharpe Ratio 1.23 Information Ratio 0 Alpha Ratio 0 Min Investment 5,000 Min SIP Investment 1,000 Exit Load 0-12 Months (1%),12 Months and above(NIL) Yield to Maturity 8.91% Effective Maturity 2 Years 7 Months 6 Days Modified Duration 2 Years 2 Months 8 Days Growth of 10,000 investment over the years.

Date Value 31 Jul 21 ₹10,000 31 Jul 22 ₹10,374 31 Jul 23 ₹11,067 31 Jul 24 ₹11,883 31 Jul 25 ₹12,943 31 Jul 26 ₹13,961 Returns for Axis Credit Risk Fund

absolute basis & more than 1 year are on CAGR (Compound Annual Growth Rate) basis. as on 21 Jan 22 Duration Returns 1 Month 0.8% 3 Month 2.9% 6 Month 4.5% 1 Year 8.2% 3 Year 8.1% 5 Year 6.9% 10 Year 15 Year Since launch 7.3% Historical performance (Yearly) on absolute basis

Year Returns 2025 8.7% 2024 8% 2023 7% 2022 4% 2021 6% 2020 8.2% 2019 4.4% 2018 5.9% 2017 6.4% 2016 9.8% Fund Manager information for Axis Credit Risk Fund

Name Since Tenure Devang Shah 15 Jul 14 12.05 Yr. Akhil Thakker 9 Nov 21 4.73 Yr. Data below for Axis Credit Risk Fund as on 30 Jun 26

Asset Allocation

Asset Class Value Cash 18.52% Equity 8.99% Debt 71.99% Other 0.5% Debt Sector Allocation

Sector Value Corporate 68.16% Cash Equivalent 18.52% Government 3.83% Credit Quality

Rating Value A 19.24% AA 60.24% AAA 20.52% Top Securities Holdings / Portfolio

Name Holding Value Quantity Jubilant Bevco Limited

Debentures | -4% ₹17 Cr 1,500 Narayana Hrudayalaya Limited

Debentures | -4% ₹15 Cr 1,500 Aditya Birla Digital Fashion Ventures Limited

Debentures | -4% ₹15 Cr 1,500 Altius Telecom Infrastructure Trust

Debentures | -4% ₹15 Cr 1,500 Vedanta Limited

Debentures | -3% ₹12 Cr 1,200 GMR Airports Limited

Debentures | -3% ₹10 Cr 1,000 Delhi International Airport Limited

Debentures | -3% ₹10 Cr 1,000 GMR Hyderabad International Airport Ltd

Debentures | -3% ₹10 Cr 1,000 Jsw Kalinga Steel Limited

Debentures | -3% ₹10 Cr 1,000 Bamboo Hotel And Global Centre (Delhi) Private Limited

Debentures | -3% ₹10 Cr 1,000 3. PGIM India Insta Cash Fund

PGIM India Insta Cash Fund

Growth Launch Date 5 Sep 07 NAV (10 Aug 26) ₹363.903 ↑ 0.08 (0.02 %) Net Assets (Cr) ₹748 on 30 Jun 26 Category Debt - Liquid Fund AMC Pramerica Asset Managers Private Limited Rating ☆☆☆☆☆ Risk Low Expense Ratio 0.25 Sharpe Ratio 2.28 Information Ratio 0.92 Alpha Ratio 0 Min Investment 5,000 Min SIP Investment 1,000 Exit Load NIL Yield to Maturity 6.57% Effective Maturity 1 Month 10 Days Modified Duration 1 Month 10 Days Growth of 10,000 investment over the years.

Date Value 31 Jul 21 ₹10,000 31 Jul 22 ₹10,368 31 Jul 23 ₹11,051 31 Jul 24 ₹11,854 31 Jul 25 ₹12,691 31 Jul 26 ₹13,494 Returns for PGIM India Insta Cash Fund

absolute basis & more than 1 year are on CAGR (Compound Annual Growth Rate) basis. as on 21 Jan 22 Duration Returns 1 Month 0.5% 3 Month 1.7% 6 Month 3.4% 1 Year 6.4% 3 Year 6.9% 5 Year 6.2% 10 Year 15 Year Since launch 7.1% Historical performance (Yearly) on absolute basis

Year Returns 2025 6.5% 2024 7.3% 2023 7% 2022 4.8% 2021 3.3% 2020 4.2% 2019 6.7% 2018 7.4% 2017 6.7% 2016 7.7% Fund Manager information for PGIM India Insta Cash Fund

Name Since Tenure Puneet Pal 16 Jul 22 4.05 Yr. Akhil Dhar 25 Feb 26 0.43 Yr. Data below for PGIM India Insta Cash Fund as on 30 Jun 26

Asset Allocation

Asset Class Value Cash 91.12% Debt 8.61% Other 0.27% Debt Sector Allocation

Sector Value Cash Equivalent 78.31% Government 12.79% Corporate 8.63% Credit Quality

Rating Value AAA 100% Top Securities Holdings / Portfolio

Name Holding Value Quantity Clearing Corporation Of India Ltd.

CBLO/Reverse Repo | -12% ₹100 Cr Bajaj Housing Finance Limited

Debentures | -6% ₹55 Cr 5,500,000 Small Industries Development Bank Of India

Debentures | -6% ₹50 Cr 5,000,000 Indian Bank

Domestic Bonds | -6% ₹50 Cr 5,000,000 India (Republic of)

- | -5% ₹44 Cr 4,500,000

↑ 4,500,000 Bank of India Ltd.

Debentures | -5% ₹43 Cr 4,350,000

↑ 4,350,000 Aditya Birla Money Limited (Frmly APollo Sindhoori Capital Investments Ltd)

Commercial Paper | -5% ₹40 Cr 4,000,000 Icici Securities Limited

Commercial Paper | -4% ₹35 Cr 3,500,000 India (Republic of)

- | -3% ₹27 Cr 2,700,000 JM Financial Services Limited

Commercial Paper | -3% ₹25 Cr 2,500,000 4. Aditya Birla Sun Life Savings Fund

Aditya Birla Sun Life Savings Fund

Growth Launch Date 16 Apr 03 NAV (10 Aug 26) ₹588.216 ↑ 0.37 (0.06 %) Net Assets (Cr) ₹17,816 on 30 Jun 26 Category Debt - Ultrashort Bond AMC Birla Sun Life Asset Management Co Ltd Rating ☆☆☆☆☆ Risk Moderately Low Expense Ratio 0.55 Sharpe Ratio 0.91 Information Ratio 0 Alpha Ratio 0 Min Investment 1,000 Min SIP Investment 1,000 Exit Load NIL Yield to Maturity 7.45% Effective Maturity 6 Months 18 Days Modified Duration 5 Months 26 Days Growth of 10,000 investment over the years.

Date Value 31 Jul 21 ₹10,000 31 Jul 22 ₹10,383 31 Jul 23 ₹11,089 31 Jul 24 ₹11,914 31 Jul 25 ₹12,876 31 Jul 26 ₹13,681 Returns for Aditya Birla Sun Life Savings Fund

absolute basis & more than 1 year are on CAGR (Compound Annual Growth Rate) basis. as on 21 Jan 22 Duration Returns 1 Month 0.6% 3 Month 1.8% 6 Month 3.4% 1 Year 6.4% 3 Year 7.3% 5 Year 6.5% 10 Year 15 Year Since launch 7.4% Historical performance (Yearly) on absolute basis

Year Returns 2025 7.4% 2024 7.9% 2023 7.2% 2022 4.8% 2021 3.9% 2020 7% 2019 8.5% 2018 7.6% 2017 7.2% 2016 9.2% Fund Manager information for Aditya Birla Sun Life Savings Fund

Name Since Tenure Sunaina Cunha 20 Jun 14 12.12 Yr. Kaustubh Gupta 15 Jul 11 15.06 Yr. Monika Gandhi 22 Mar 21 5.36 Yr. Data below for Aditya Birla Sun Life Savings Fund as on 30 Jun 26

Asset Allocation

Asset Class Value Cash 33.37% Debt 66.63% Debt Sector Allocation

Sector Value Corporate 71.59% Government 18.6% Cash Equivalent 9.81% Credit Quality

Rating Value AA 32.96% AAA 67.04% Top Securities Holdings / Portfolio

Name Holding Value Quantity India (Republic of)

- | -5% ₹842 Cr 85,000,000 National Bank for Agriculture and Rural Development

Domestic Bonds | -4% ₹729 Cr 15,300 Shriram Finance Limited

Debentures | -3% ₹608 Cr 60,000 Bharti Telecom Limited

Debentures | -2% ₹396 Cr 40,000 Muthoot Finance Limited

Debentures | -2% ₹349 Cr 35,000 Indusind Bank Ltd.

Debentures | -2% ₹345 Cr 7,100 Vedanta Limited

Debentures | -2% ₹328 Cr 32,500 Mankind Pharma Limited

Debentures | -2% ₹320 Cr 32,000 Avanse Financial Services Limited

Debentures | -2% ₹300 Cr 30,000 Power Finance Corporation Limited

Debentures | -2% ₹297 Cr 30,000 5. Aditya Birla Sun Life Money Manager Fund

Aditya Birla Sun Life Money Manager Fund

Growth Launch Date 13 Oct 05 NAV (10 Aug 26) ₹397.18 ↑ 0.29 (0.07 %) Net Assets (Cr) ₹27,383 on 30 Jun 26 Category Debt - Money Market AMC Birla Sun Life Asset Management Co Ltd Rating ☆☆☆☆☆ Risk Low Expense Ratio 0.35 Sharpe Ratio 0.69 Information Ratio 0 Alpha Ratio 0 Min Investment 1,000 Min SIP Investment 1,000 Exit Load NIL Yield to Maturity 6.95% Effective Maturity 6 Months 29 Days Modified Duration 6 Months 25 Days Growth of 10,000 investment over the years.

Date Value 31 Jul 21 ₹10,000 31 Jul 22 ₹10,381 31 Jul 23 ₹11,117 31 Jul 24 ₹11,961 31 Jul 25 ₹12,918 31 Jul 26 ₹13,720 Returns for Aditya Birla Sun Life Money Manager Fund

absolute basis & more than 1 year are on CAGR (Compound Annual Growth Rate) basis. as on 21 Jan 22 Duration Returns 1 Month 0.6% 3 Month 1.9% 6 Month 3.4% 1 Year 6.3% 3 Year 7.3% 5 Year 6.6% 10 Year 15 Year Since launch 6.8% Historical performance (Yearly) on absolute basis

Year Returns 2025 7.4% 2024 7.8% 2023 7.4% 2022 4.8% 2021 3.8% 2020 6.6% 2019 8% 2018 7.9% 2017 6.8% 2016 7.7% Fund Manager information for Aditya Birla Sun Life Money Manager Fund

Name Since Tenure Kaustubh Gupta 15 Jul 11 15.06 Yr. Anuj Jain 22 Mar 21 5.36 Yr. Mohit Sharma 1 Apr 17 9.34 Yr. Data below for Aditya Birla Sun Life Money Manager Fund as on 30 Jun 26

Asset Allocation

Asset Class Value Cash 65.54% Debt 34.46% Debt Sector Allocation

Sector Value Corporate 55.48% Cash Equivalent 32.51% Government 12.01% Credit Quality

Rating Value AAA 100% Top Securities Holdings / Portfolio

Name Holding Value Quantity Indusind Bank Ltd.

Debentures | -5% ₹1,393 Cr 29,000 Indusind Bank Ltd.

Debentures | -4% ₹1,112 Cr 22,900 Axis Bank Ltd.

Debentures | -3% ₹922 Cr 19,000 Federal Bank Ltd.

Debentures | -3% ₹911 Cr 19,000 Gujarat State Development Loans

Sovereign Bonds | -3% ₹797 Cr 79,327,600 Karur Vysya Bank Ltd.

Debentures | -2% ₹479 Cr 10,000 Tbill

Sovereign Bonds | -1% ₹396 Cr 40,000,000 Indian Bank

Domestic Bonds | -1% ₹392 Cr 8,000

↑ 8,000 7.49% Gujarat Sgs 2026

Sovereign Bonds | -1% ₹326 Cr 32,500,000 7.43% Gujarat Sgs 2027

Sovereign Bonds | -1% ₹247 Cr 24,500,000

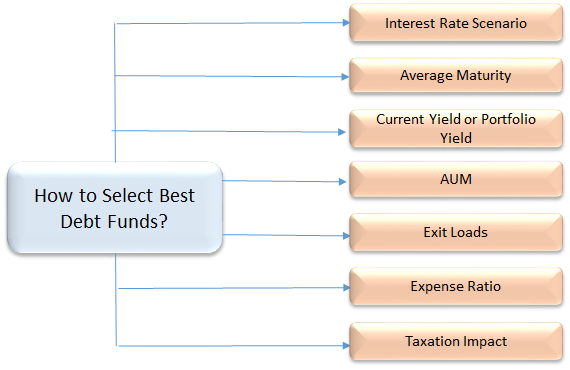

சிறந்த கடன் பரஸ்பர நிதிகளை எவ்வாறு மதிப்பிடுவது

நீங்கள் முதலீடு செய்ய விரும்பும் சிறந்த கடன் நிதிகளைத் தேர்ந்தெடுப்பதற்கு, சராசரி முதிர்வு, கடன் தரம், AUM, செலவு விகிதம், வரி தாக்கம் போன்ற சில முக்கியமான அளவுருக்களைக் கருத்தில் கொள்வது அவசியம். ஆழமாகப் பார்ப்போம். -

1. சராசரி முதிர்வு/காலம்

சராசரி முதிர்வு என்பது கடன் நிதிகளில் இன்றியமையாத அளவுருவாகும், இது சில நேரங்களில் முதலீட்டாளர்களால் கவனிக்கப்படுவதில்லை, இதில் உள்ள அபாயங்களைக் கருத்தில் கொள்ளாமல் நீண்ட காலத்திற்கு முதலீடு செய்கிறார்கள். முதலீட்டாளர்கள் தங்கள் கடன் நிதி முதலீட்டை அதன் முதிர்வு காலத்தின் அடிப்படையில் தீர்மானிக்க வேண்டும், முதலீட்டின் காலத்தை கடன் நிதியின் முதிர்வு காலத்துடன் பொருத்துவது நீங்கள் தேவையற்ற ரிஸ்க் எடுக்காமல் இருப்பதை உறுதி செய்வதற்கான ஒரு சிறந்த வழியாகும். எனவே, கடன் நிதிகளில் உகந்த ரிஸ்க் வருவாயை இலக்காகக் கொண்டு முதலீடு செய்வதற்கு முன், கடன் நிதியின் சராசரி முதிர்ச்சியை அறிந்து கொள்வது நல்லது. சராசரி முதிர்ச்சியைப் பார்ப்பது (காலம் ஒத்த காரணி) முக்கியமானது, எடுத்துக்காட்டாக, ஒரு திரவ நிதி சராசரியாக இரண்டு நாட்கள் முதல் ஒரு மாதம் வரை முதிர்ச்சியைக் கொண்டிருக்கலாம், இது தேடும் முதலீட்டாளருக்கு இது ஒரு சிறந்த வழி என்று அர்த்தம். இரண்டு நாட்களுக்கு பணத்தை முதலீடு செய்ய. இதேபோல், நீங்கள் ஒரு வருட கால அளவைப் பார்த்தால்முதலீட்டுத் திட்டம் பின்னர், ஒரு குறுகிய கால கடன் நிதி சிறந்ததாக இருக்கும்.

2. வட்டி விகிதம் காட்சி

வட்டி விகிதங்கள் மற்றும் அதன் ஏற்ற இறக்கங்களால் பாதிக்கப்படும் கடன் நிதிகளில் சந்தை சூழலைப் புரிந்துகொள்வது மிகவும் முக்கியமானது. பொருளாதாரத்தில் வட்டி விகிதம் உயரும் போது, பத்திர விலை குறைகிறது மற்றும் நேர்மாறாகவும். மேலும், வட்டி விகிதங்கள் உயரும் நேரத்தில், பழைய பத்திரங்களை விட அதிக மகசூலுடன் சந்தையில் புதிய பத்திரங்கள் வெளியிடப்படுகின்றன, இதனால் பழைய பத்திரங்கள் குறைந்த மதிப்புள்ளவை. எனவே, முதலீட்டாளர்கள் சந்தையில் புதிய பத்திரங்களை நோக்கி அதிகம் ஈர்க்கப்படுகிறார்கள், மேலும் பழைய பத்திரங்களின் மறு விலை நிர்ணயமும் நடைபெறுகிறது. ஒரு கடன் நிதியானது அத்தகைய "பழைய பத்திரங்களுக்கு" வெளிப்பாடு இருந்தால், வட்டி விகிதங்கள் உயரும் போது,இல்லை கடன் நிதி எதிர்மறையாக பாதிக்கப்படும். மேலும், கடன் நிதிகள் வட்டி விகித ஏற்ற இறக்கங்களுக்கு ஆளாவதால், இது ஃபண்ட் போர்ட்ஃபோலியோவில் உள்ள அடிப்படைப் பத்திரங்களின் விலைகளைத் தொந்தரவு செய்கிறது. உதாரணமாக, வட்டி விகிதங்கள் உயரும் காலங்களில் நீண்ட கால கடன் நிதிகள் அதிக ஆபத்தில் உள்ளன. இந்த நேரத்தில் குறுகிய கால முதலீட்டுத் திட்டத்தை உருவாக்குவது உங்கள் வட்டி விகித அபாயங்களைக் குறைக்கும்.

ஒருவர் வட்டி விகிதங்களைப் பற்றி நன்கு அறிந்திருந்தால், அதைக் கண்காணிக்க முடியும் என்றால், ஒருவர் இதைப் பயன்படுத்திக் கொள்ளலாம். வீழ்ச்சியடைந்த வட்டி விகித சந்தையில், நீண்ட கால கடன் நிதிகள் ஒரு நல்ல தேர்வாக இருக்கும். இருப்பினும், வட்டி விகிதங்கள் உயரும் காலங்களில், குறுகிய கால நிதிகள் போன்ற குறுகிய சராசரி முதிர்வுகளைக் கொண்ட ஃபண்டுகளில் இருப்பது புத்திசாலித்தனமாக இருக்கும்.அல்ட்ரா குறுகிய கால நிதி அல்லது திரவ நிதிகள் கூட.

3. தற்போதைய மகசூல் அல்லது போர்ட்ஃபோலியோ விளைச்சல்

ஈவுத்தொகை என்பது போர்ட்ஃபோலியோவில் உள்ள பத்திரங்களால் உருவாக்கப்படும் வட்டி வருமானத்தின் அளவீடு ஆகும். கடன் அல்லது பத்திரங்களில் முதலீடு செய்யும் நிதிகள் அதிகம்கூப்பன் விகிதம் (அல்லது மகசூல்) அதிக ஒட்டுமொத்த போர்ட்ஃபோலியோ விளைச்சலைக் கொண்டிருக்கும். முதிர்ச்சிக்கான மகசூல் (ytm) ஒரு கடன் பரஸ்பர நிதி நிதியின் இயங்கும் வருவாயைக் குறிக்கிறது. YTM அடிப்படையில் கடன் நிதிகளை ஒப்பிடும் போது, கூடுதல் மகசூல் எவ்வாறு உருவாக்கப்படுகிறது என்பதையும் பார்க்க வேண்டும். இது குறைந்த போர்ட்ஃபோலியோ தரத்தின் விலையில் உள்ளதா? அவ்வளவு நல்ல தரமில்லாத கருவிகளில் முதலீடு செய்வது அதன் சொந்த சிக்கல்களைக் கொண்டுள்ளது. அத்தகைய பத்திரங்கள் அல்லது பத்திரங்களைக் கொண்ட கடன் நிதியில் முதலீடு செய்வதை நீங்கள் முடிக்க விரும்பவில்லைஇயல்புநிலை பின்னர். எனவே, எப்போதும் போர்ட்ஃபோலியோ விளைச்சலைப் பார்த்து, அதை கிரெடிட் தரத்துடன் சமநிலைப்படுத்துங்கள்.

4. போர்ட்ஃபோலியோவின் கடன் தரம்

சிறந்த கடன் நிதிகளில் முதலீடு செய்வதற்கு, கடன் பத்திரங்கள் மற்றும் கடன் பத்திரங்களின் கடன் தரத்தை சரிபார்ப்பது இன்றியமையாத அளவுருவாகும். பணத்தைத் திருப்பிச் செலுத்தும் திறனின் அடிப்படையில் பல்வேறு ஏஜென்சிகளால் கடன் மதிப்பீடுகள் பத்திரங்களுக்கு வழங்கப்படுகின்றன. AAA மதிப்பீட்டைக் கொண்ட ஒரு பத்திரம் சிறந்த கடன் மதிப்பீடாகக் கருதப்படுகிறது மற்றும் பாதுகாப்பான மற்றும் பாதுகாப்பான முதலீட்டையும் குறிக்கிறது. ஒருவர் உண்மையிலேயே பாதுகாப்பை விரும்பி, சிறந்த கடன் நிதியைத் தேர்ந்தெடுப்பதில் முக்கிய அளவுருவாகக் கருதினால், மிக உயர்தரக் கடன் கருவிகளைக் கொண்ட (AAA அல்லது AA+) நிதியில் சேர்வதே விருப்பமான விருப்பமாக இருக்கலாம்.

5. நிர்வாகத்தின் கீழ் உள்ள சொத்துக்கள் (AUM)

சிறந்த கடன் நிதிகளைத் தேர்ந்தெடுக்கும்போது கருத்தில் கொள்ள வேண்டிய முதன்மையான அளவுரு இதுவாகும். AUM என்பது அனைத்து முதலீட்டாளர்களாலும் ஒரு குறிப்பிட்ட திட்டத்தில் முதலீடு செய்யப்படும் மொத்தத் தொகையாகும். முதல், பெரும்பாலானபரஸ்பர நிதிமொத்த AUM கடன் நிதிகளில் முதலீடு செய்யப்படுகிறது, முதலீட்டாளர்கள் கணிசமான AUM ஐக் கொண்ட திட்ட சொத்துக்களை தேர்ந்தெடுக்க வேண்டும். கார்ப்பரேட் நிறுவனங்களுக்கு அதிக வெளிப்பாட்டைக் கொண்ட ஃபண்டில் இருப்பது ஆபத்தானதாக இருக்கலாம், ஏனெனில் அவர்கள் திரும்பப் பெறுவது பெரியதாக இருக்கலாம், இது ஒட்டுமொத்த நிதி செயல்திறனைப் பாதிக்கலாம்.

6. செலவு விகிதம்

கடன் நிதிகளில் கருத்தில் கொள்ள வேண்டிய ஒரு முக்கியமான காரணி அதன் செலவு விகிதம் ஆகும். அதிக செலவு விகிதம் நிதியின் செயல்திறனில் பெரிய தாக்கத்தை உருவாக்குகிறது. எடுத்துக்காட்டாக, திரவ நிதிகள் 50 பிபிஎஸ் வரை குறைந்த செலவின விகிதங்களைக் கொண்டுள்ளன (பிபிஎஸ் என்பது வட்டி விகிதங்களை அளவிடுவதற்கான ஒரு அலகு, இதில் ஒரு பிபிஎஸ் 1/100 வது 1% ஆகும்), மற்ற கடன் நிதிகள் 150 பிபிஎஸ் வரை வசூலிக்கலாம். எனவே ஒரு கடன் பரஸ்பர நிதிக்கு இடையே தேர்வு செய்ய, மேலாண்மை கட்டணம் அல்லது நிதி இயங்கும் செலவைக் கருத்தில் கொள்வது முக்கியம்.

7. வரிவிதிப்பு பாதிப்புகள்

கடன் நிதிகள் நீண்ட கால மூலதன ஆதாயங்களின் (3 ஆண்டுகளுக்கு மேல்) குறியீட்டு பலன்களுடன் பலன்களை வழங்குகின்றன. மற்றும் குறுகிய கால மூலதன ஆதாயங்கள் (3 ஆண்டுகளுக்கு குறைவாக) 30% வரி விதிக்கப்படுகிறது.

ஒரு முதலீட்டாளராக கருத்தில் கொள்ள வேண்டிய விஷயங்கள்

1. நிதி நோக்கங்கள்

பல்வேறு வகையான பத்திரங்களின் பன்முகப்படுத்தப்பட்ட போர்ட்ஃபோலியோவைப் பராமரிப்பதன் மூலம் உகந்த வருமானத்தை ஈட்டுவதை டெப்ட் ஃபண்ட் நோக்கமாகக் கொண்டுள்ளது. அவர்கள் யூகிக்கக்கூடிய வகையில் செயல்படுவார்கள் என்று எதிர்பார்க்கலாம். இந்தக் காரணத்தினால்தான், கடன் நிதிகள் பழமைவாத முதலீட்டாளர்களிடையே பிரபலமாக உள்ளன.

2. நிதி வகைகள்

கடன் நிதிகள் மேலும் திரவ நிதிகள் போன்ற பல்வேறு வகைகளாக பிரிக்கப்படுகின்றன,மாதாந்திர வருமானத் திட்டம் (எம்ஐபி), நிலையான முதிர்வுத் திட்டங்கள் (எஃப்எம்பி),டைனமிக் பாண்ட் நிதிகள், வருமான நிதிகள், கடன் வாய்ப்பு நிதிகள், GILT நிதிகள், குறுகிய கால நிதிகள் மற்றும் தீவிர குறுகிய கால நிதிகள்.

3. அபாயங்கள்

கடன் நிதிகள் அடிப்படையில் வட்டி விகித ஆபத்து, கடன் ஆபத்து மற்றும்நீர்மை நிறை ஆபத்து. ஒட்டுமொத்த வட்டி விகித இயக்கங்கள் காரணமாக நிதி மதிப்பு மாறலாம். வழங்குநரால் வட்டி மற்றும் அசலை செலுத்துவதில் இயல்புநிலை ஏற்படும் அபாயம் உள்ளது. தேவை இல்லாததால், நிதி மேலாளரால் அடிப்படைப் பாதுகாப்பை விற்க முடியாமல் போகும்போது பணப்புழக்க ஆபத்து ஏற்படுகிறது.

4. செலவு

உங்கள் பணத்தை நிர்வகிக்க கடன் நிதிகள் செலவு விகிதத்தை வசூலிக்கின்றன. அது இப்போது வரைசெபி செலவு விகிதத்தின் உச்ச வரம்பை 2.25% ஆகக் கட்டாயப்படுத்தியிருந்தது (ஒழுங்குமுறைகளுடன் அவ்வப்போது மாறலாம்.).

5. முதலீட்டு அடிவானம்

3 மாதங்கள் முதல் 1 வருடம் வரையிலான முதலீடு திரவ நிதிகளுக்கு ஏற்றதாக இருக்கும். உங்களிடம் 2 முதல் 3 ஆண்டுகள் வரை நீண்ட கால அவகாசம் இருந்தால், நீங்கள் குறுகிய கால பத்திர நிதிகளுக்கு செல்லலாம்.

6. நிதி இலக்குகள்

கூடுதல் வருமானம் ஈட்டுதல் அல்லது பணப்புழக்கம் போன்ற பல்வேறு இலக்குகளை அடைய கடன் நிதிகள் பயன்படுத்தப்படலாம்.

ஆன்லைனில் சிறந்த கடன் நிதிகளில் முதலீடு செய்வது எப்படி?

Fincash.com இல் வாழ்நாள் முழுவதும் இலவச முதலீட்டுக் கணக்கைத் திறக்கவும்.

உங்கள் பதிவு மற்றும் KYC செயல்முறையை முடிக்கவும்

ஆவணங்களைப் பதிவேற்றவும் (PAN, ஆதார் போன்றவை).மேலும், நீங்கள் முதலீடு செய்ய தயாராக உள்ளீர்கள்!

முடிவுரை

உங்கள் பணத்தை முதலீடு செய்வதற்கும், உங்களுக்கான பொருத்தமான பொருளைத் தேர்ந்தெடுப்பதன் மூலம் வழக்கமான அடிப்படையில் வருமானம் ஈட்டுவதற்கும் கடன் நிதிகள் சிறந்த வழிகளில் ஒன்றாகும்.ஆபத்து விவரக்குறிப்பு. எனவே, நிலையான வருமானத்தை ஈட்ட அல்லது கடன் சந்தைகளைப் பயன்படுத்திக் கொள்ள விரும்பும் முதலீட்டாளர்கள், 2022 - 2023க்கான மேற்கூறிய சிறந்த கடன் நிதிகளைக் கருத்தில் கொண்டு முதலீடு செய்யத் தொடங்கலாம்!_

இங்கு வழங்கப்பட்ட தகவல்கள் துல்லியமானவை என்பதை உறுதிப்படுத்த அனைத்து முயற்சிகளும் மேற்கொள்ளப்பட்டுள்ளன. இருப்பினும், தரவின் சரியான தன்மை குறித்து எந்த உத்தரவாதமும் அளிக்கப்படவில்லை. முதலீடு செய்வதற்கு முன் திட்டத் தகவல் ஆவணத்துடன் சரிபார்க்கவும்.

You Might Also Like

AMFI Registration No. 112358 | CIN: U74999MH2016PTC282153

Shepard Technologies Pvt. Ltd. (with ARN code 112358) makes no warranties or representations, express or implied, on products offered through the platform. It accepts no liability for any damages or losses, however caused, in connection with the use of, or on the reliance of its product or related services. Terms and conditions of the website are applicable.

©2026 Shepard Technologies Private Limited. All Rights Reserved

The article is nice and informative but it could be in more simple words because lot of people have much less knowledge in such sector